Mada "Naqd" Service (Purchase with Cash-back) Business Rules

No: 371000016319 Date(g): 21/11/2015 | Date(h): 10/2/1437 Document References

Name Version SPAN Purchase with Cashback - Requirements Specification V1.1 SPAN Pricing - Business Requirement MoSCoW Template.doc V 0.03 SPAN Business Strategy V1.4 SPAN Daily/Monthly Reconciliation Reports - Revised June 2013 1. Introduction

The Saudi Arabian Payments Network (SPAN) supports all card payments within the Kingdom and is a key component in the Saudi Arabian National Payments Strategy delivered through the IPSS. The SPAN Business Strategy (SPAN 2016 - Driving Change) is designed to position SPAN as the 'First Payment choice in the Kingdom of Saudi Arabia'. Driven by the IPSS objective of reducing the volume and velocity of cash in the kingdom, the SPAN scheme will target the reduction of cash in the kingdom from over 94% of retail payment transaction volume, to less than 70% by 2020.

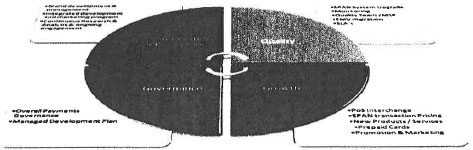

The SPAN Business Strategy defines the development and change program Into four key dimensions:

a. Quality initiatives, designed to improve the overall service level and performance of the scheme b. Growth Initiatives, designed to extend the reach of cashless retail payment services within the kingdom and to stimulate increased usage of card payment services among existing SPAN cardholders c. Governance of the SPAN Scheme and development programme, to ensure appropriate development and management of stakeholder interests d. Communications Initiatives, to ensure a consistent level of stakeholder education and understanding of the SPAN vision, mission and deliverables, optimization of the scheme promotional and marketing initiatives and a clear understanding of the operational and regulatory obligations of scheme participants.

Figure 1: 'SPAN 2016 - Driving Change' program outline

Central to the development of the SPAN service is the ongoing development of new business services which:

1. Support the strategic direction of the IPSS and the SPAN Business Strategy - 2016 2. Offer added value to the key stakeholders (Merchant, Card Issuer and Card Acquirer) 3. Offers value to the Card holder

Naqd Service (Cash-back with Purchase) at Point of Sale generates the following opportunities:

○ Encourages cardholders to use PoS functionality as a source of multiple Card based services ○ Migrates some traffic away from (an already busy) ATM network ○ Provides an opportunity for Merchants to offload (expensive) cash ○ Allows Card Acquirers sell the benefits of PoS, by including Cash-back as an additional service suite to the Merchant

Naqd Service at PoS Is a common feature in retail (card) payment markets In Europe, Asia, US and Australia, and is acknowledged as a material feature of progressive card-based retail payments systems.

International analysis suggests that Cash-back with purchase at point of sale can be a feature of (typically) 5% to 8% of card point-of-sale transactions.

2. Naqd Service Business Rules

2.1 Service Availability

1. The 'Naqd Service' will be offered as a SPAN/mada Scheme service

2. The service will be (technically) available on all SPAN/mada branded cards

3. Naqd will be available at all SPAN/mada Merchant terminals.

a. The Acquirer will have the capacity to disable the Naqd facility at any of their Merchants by assigning the Merchant to the appropriate 'TMS Group', which excludes the Naqd feature

4. Naqd will only be available to cardholders if conducted as part of a SPAN/mada purchase transaction

a. The Total Value of the transaction will be identified in field DE04 b. The Naqd (Cash-back) element of the transaction will be Identified in field DE54 c. A Naqd (Cash-back) only transaction will be Identifiable and declined by the Issuer (i.e. DE04 = DE54 > 0) d. The processing code, field DE03 carries the processing code 090000

2.2 Transaction Limits

5. There will be no maximum number of transactions per day on which Naqd could be requested or authorised (subject to available funds)

6. The scheme will operate to a parameterised minimum and maximum value for cash-back.

a. Minimum Value - SAR 1 b. Maximum Value - SAR 400 per day c. Cash-back values will be calculated and permitted to two places of decimals

The maximum value will be calculated and applied daily, subject to available funds and will be managed by the Card Issuer

7. When a Naqd transaction is requested, the request will be evaluated at three levels:

a. The Acquirer (Terminal) will check to confirm that the individual transaction(s) for Purchase and for Naqd don't exceed SAR 60,000 and SAR 400 respectively b. The SPAN Switch will check to ensure the total value of the transaction does not exceed the PoS limit (DE04 <= SAR 60,400) c. The Issuer will check to ensure the cumulative Purchase value and/or the Cash-back value doesn't exceed the daily limit(s)

8. Daily limits will be defined on the calendar day, typically, but not mandated, from 00:00:00 to 23:59:59

9. Transactions containing values that cause either the cumulative daily PoS Purchase limit of up to SAR 60,000 or the cumulative daily Naqd limit of SAR 400 to be exceeded, will be declined in total

10. Naqd 'Cash-back' values will form part of the revised cumulative total PoS value limit of SAR 60,400 per day*

2.3 Naqd Transaction Authorization

11. A Naqd 'Cash-back' element will only be permitted on a transaction that has received (online) positive authorization from the Issuer

12. Where 'off-line transaction functionality' Is available, Naqd will not be permitted.

2.4 Commercial Model

13. Naqd will operate as a 'fee-free' transaction to the Card Issuer, Transaction Acquirer, Merchant and Cardholder. No unique SPAN switch fees will be applied by the scheme to the Naqd 'Cash-back' element of the Point of Sale (PoS) transaction.

a. The Issuer and Acquirer fees applied at the SPAN switch will reflect the standard rate for the card (i.e. one Authorization Fee and a split Settlement Fee for the overall Purchase & Naqd 'Cash-back' transaction) b. Interchange Fees will apply for the Purchase element only (i.e. the value of field DE04-DE54), based on Table 1 below: (See SPAN/mada Charging Policy for details)

Table 1: SPAN PoS Interchange Fees (Acquirer pays Issuer)

Interchange Value Band From To SPAN Interchange Band 1 SAR 0.00 SAR 1,000 0.4% (40bp) Band 2 SAR 1.000.01 SAR 60,000.00 SAR 4.00 c. MSC charged by the SPAN Acquirer to the Merchant on the total transaction will be subject to the normal SPAN Maximum, based on the Purchase element only (i.e. the value of field DE04-DE54.

Table 2: SPAN PoS MSC Maximum Fees (Subject to bi-lateral negotiation between Acquirer & Merchant)

Merchant Services Commission (MSC) Value Bands From To SPAN MSC Band 1 SAR 0.00 SAR 5,000.00 (approx.) 0.8% (80bp) max Band 2 SAR 5,000.01 (approx.) SAR 60,000.00 SAR 40.00 max The SAR5,000 reference Is Indicative, since MSC rate Is negotiable between Acquirer and Merchant, but still subject to SAR 40 max

2.5 PoS Terminal Output

14. SPAN PoS Terminal will be configured to generate a counterfoil/transaction confirmation which includes:

a. Purchase Value (DE04 - DE54) b. Naqd (Cash-back) value (DE54) c. Total transaction value (DE04)

15. The Naqd 'Cash-back' element on the 'receipt' will be situated close to a cardholder signature panel where the cardholder will be asked to sign to confirm receipt of the cash as this will help in the event of a dispute

Promotional material should encourage the Merchant to confirm the Naqd element on the merchant receipt copy, which should then be signed by the cardholder, as this will help in the event of a dispute.

2.6 Bank to Customer Reporting

16. Transaction Reporting on Statements:

a. The cardholder statement will post a single transaction for the full value of the Purchase and Naqd (Cash-back) value (i.e. field DE04). b. The Transaction narrative on the statement will detail the value of the Cash-back element, (DE54) and the value of the Purchase element (DE04 - DE54) c. SMS messages to the cardholder after execution of a transaction shall adopt a standard message, which will be Issued In both Arabic and English.

17. The SMS (transaction confirmation) narrative will read:

Your account XXXX has been debited for SAR NNN.NN(DE04) Including purchase value SAR XXX.XX (DE04-DE54) and Naqd value YYY. YY (DE54) at <Merchant Name> on dd.mm.yyyy at hh:mm

2.7 Naqd (Cash-back with Purchase) - Transaction Declines and Reason Codes

18. Decline reason codes will be issued from the acquirer to the merchant (via SPAN) where a requested transaction has been denied by the issuer. Where relevant, a transaction will be declined In whole (i.e. both the Purchase and the Cash-back element will be declined).

19. The standard reasons codes apply, as defined in the Decline reason codes will be as follows:

a. DE 39 (SPAN Technical Books, Part 4, MBI p 106)

i. Reason Code 110 - Invalid Amount (where the cumulative purchase amount exceeds the dally limit) ii. Reason Code 121 - Exceeds Withdrawal Amount (where the cumulative Naqd cash-back amount exceeds the daily limit) iii. No additional / new decline codes are added or changed and all other decline codes remain applicable where appropriate and are unchanged

2.8 Naqd (Cash-back with Purchase) - Transaction Reversals

20. A PoS transaction reversal will be effected when:

a. The Merchant cancels the transaction within 60 seconds of approval or b. The SPAN switch determines that the transaction is incomplete (timed out)

The SPAN Operating Standards and Procedures V 6.0 section 5.4 (page 106) outlines the relevant procedures and processes.

21. A Purchase with Cash-back transaction will also be reversed in these conditions. In such cases, the full amount of the transaction will be reversed (DE04) prior to the Merchant completing the transaction or issuing the cash. No further action is required.

2.9 Naqd (Cash-back with Purchase) - Transaction Refunds

22. Transaction refunds will be managed as normal through the Complaints Processing System (CPS - see CPS Claims Officer Rulebook).

Where appropriate for refund and following CPS due process, only the Purchase Amount of the transaction (DE04 - DE54) will be subject to refund. The Naqd Cash-back element will not be subject to refund.

2.10 Bank to Merchant Reporting

23. The Merchant Bank and the Merchant will receive information relating to the 'total value of Cash-back processed per terminal'.

This value will be carried in field DE124.7 and will support Merchant and Terminal reconciliation. (See SPAN Technical Books v 5.4: Part 4: MBI p163)

2.11 Bank Reporting

24. SAMA / SPAN Reporting schedules will uniquely identify transactions which included cash- back.

25. The 'Interchange Fee' report for each bank will show the number of 'Purchase with Cash- back' transactions effected by the issuer, falling into each of the Interchange bands. Transactions will be allocated to an interchange band based on the value of the purchase component only (DE04-DE54)

2.12 (Internal) SAMA Reporting

26. No additional changes to the current SAMA internal reporting suite, which carries a 'whole count' reference field for Naqd (Purchase with Cash-back) transactions, is required.